VA Home Loans: Simplifying the Home Buying Process for Armed Force Employee

VA Home Loans: Simplifying the Home Buying Process for Armed Force Employee

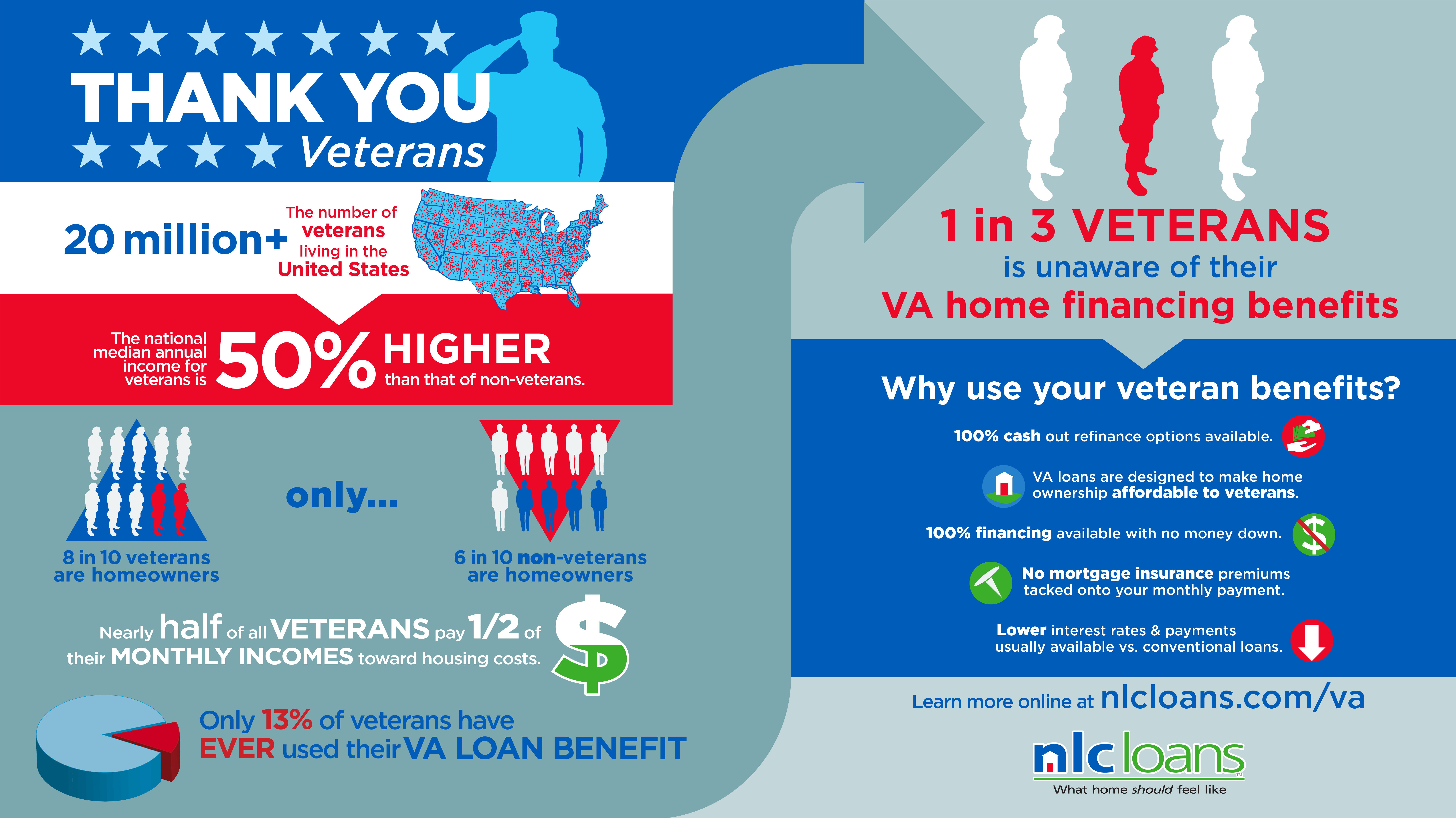

Blog Article

Optimizing the Benefits of Home Loans: A Step-by-Step Strategy to Securing Your Suitable Property

Browsing the complicated landscape of home finances needs a methodical approach to make certain that you safeguard the property that straightens with your economic goals. To truly take full advantage of the benefits of home lendings, one must consider what actions follow this foundational job.

Comprehending Mortgage Basics

Understanding the principles of home loans is essential for any person taking into consideration buying a residential property. A home mortgage, commonly referred to as a mortgage, is an economic product that allows people to borrow cash to get realty. The borrower consents to pay back the car loan over a specified term, normally ranging from 15 to three decades, with rate of interest.

Trick elements of home car loans consist of the primary quantity, rates of interest, and payment schedules. The principal is the quantity obtained, while the interest is the price of borrowing that amount, expressed as a portion. Rate of interest can be fixed, continuing to be continuous throughout the financing term, or variable, varying based upon market problems.

Additionally, borrowers should know different types of mortgage, such as traditional lendings, FHA lendings, and VA car loans, each with distinct eligibility standards and advantages. Recognizing terms such as down payment, loan-to-value ratio, and personal home mortgage insurance (PMI) is also important for making educated choices. By grasping these basics, potential property owners can browse the intricacies of the home loan market and determine choices that line up with their monetary objectives and property aspirations.

Evaluating Your Financial Situation

Assessing your financial circumstance is an important action before getting started on the home-buying journey. Next, checklist all month-to-month costs, ensuring to account for fixed costs like lease, utilities, and variable expenditures such as grocery stores and home entertainment.

After developing your revenue and costs, determine your debt-to-income (DTI) proportion, which is important for lending institutions. This proportion is computed by splitting your complete monthly financial obligation payments by your gross month-to-month revenue. A DTI ratio below 36% is usually considered desirable, indicating that you are not over-leveraged.

Furthermore, analyze your credit rating, as it plays an essential duty in securing beneficial financing terms. A higher credit report can lead to lower interest prices, inevitably conserving you cash over the life of the lending.

Checking Out Loan Choices

With a clear photo of your monetary situation developed, the next action involves checking out the various lending choices offered to possible homeowners. Recognizing the different kinds of mortgage is essential in selecting the ideal one for your needs.

Traditional fundings are conventional funding approaches that generally call for a greater credit report score and deposit yet deal competitive rate of interest. Alternatively, government-backed loans, such as FHA, VA, and USDA fundings, accommodate details teams and often require lower down repayments and credit report, making them available for novice purchasers or those with restricted funds.

One more choice is variable-rate mortgages (ARMs), which feature lower initial rates that adjust after a given period, potentially bring about significant financial savings. Fixed-rate home mortgages, on the various other hand, provide security with a consistent rate of interest throughout the car loan term, securing you against market fluctuations.

In addition, take into consideration the financing term, which usually varies from 15 to thirty years. Shorter terms might have greater regular monthly payments yet can conserve you rate of interest in time. By carefully evaluating these alternatives, you can make an educated choice that lines up with your economic goals and homeownership desires.

Preparing for the Application

Effectively preparing for the application procedure is important for protecting a home loan. A solid credit score is important, as it influences the car loan quantity and passion prices available to you.

Next, gather essential documentation. Common demands include recent pay stubs, income tax return, financial institution declarations, and evidence Full Article of properties. Organizing these documents in advancement can substantially expedite the application process. Additionally, consider obtaining a pre-approval from loan providers. When making an offer on a residential property., this not just gives a clear understanding of your loaning capability however likewise enhances your setting.

Additionally, establish your budget by factoring in not just the financing quantity however also home taxes, insurance policy, and maintenance prices. Acquaint on your own with different lending kinds and their respective terms, as this expertise will encourage you to make educated choices during the application procedure. By taking these proactive actions, you will improve your readiness and boost your chances of safeguarding the home funding that ideal fits your requirements.

Closing the Bargain

Throughout the closing meeting, you will certainly examine and sign different records, such as the financing estimate, closing disclosure, and mortgage agreement. It is important to extensively understand these files, as they outline the funding terms, settlement timetable, and closing costs. Take the time to check my site ask your loan provider or realty representative any kind of questions you may have to avoid misconceptions.

Once all papers are authorized and funds are transferred, you will certainly obtain the keys to your brand-new home. Remember, closing prices can differ, visit their website so be gotten ready for expenditures that might include evaluation costs, title insurance policy, and attorney fees - VA Home Loans. By remaining arranged and educated throughout this process, you can guarantee a smooth change right into homeownership, making best use of the benefits of your home mortgage

Conclusion

Finally, making best use of the advantages of mortgage demands an organized approach, encompassing a complete analysis of economic circumstances, exploration of diverse lending choices, and precise preparation for the application process. By adhering to these steps, prospective property owners can improve their possibilities of protecting desirable funding and attaining their home ownership goals. Ultimately, mindful navigating of the closing procedure additionally strengthens a successful transition into homeownership, ensuring lasting financial stability and contentment.

Browsing the facility landscape of home lendings calls for a systematic method to ensure that you safeguard the home that lines up with your monetary goals.Comprehending the principles of home loans is essential for any individual thinking about purchasing a residential property - VA Home Loans. A home car loan, usually referred to as a home loan, is a financial item that allows people to borrow money to buy genuine estate.Additionally, debtors should be mindful of various kinds of home lendings, such as standard car loans, FHA loans, and VA finances, each with distinct eligibility standards and advantages.In final thought, maximizing the benefits of home finances necessitates a methodical strategy, encompassing an extensive analysis of economic situations, exploration of varied financing options, and precise prep work for the application procedure

Report this page